How would the Finance Act, 2020 affect my business? What impact would it have on the prices of goods and services? These are questions that the recently signed finance bill have raised. The answers to these questions are provided in this article. Anyway, before we proceed here is a brief preamble.

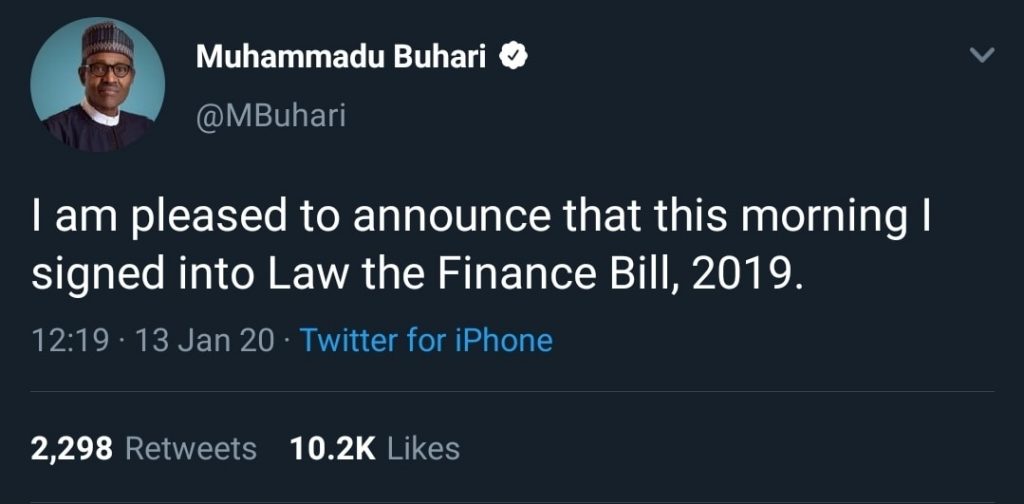

The Nigerian President, President Muhammadu Buhari, signed the 2019 Finance Bill into law on the 13th of January, 2020.

According to the government, the new tax law is intended to support small and medium scale enterprises, as well as to finance key government projects, especially in the areas of health, education, and critical infrastructure.

However, Mrs Zainab Shamsuna Ahmed, the Minister of Finance, mentioned on Tuesday, 14th January, that the date for the implementation of the newly signed Finance bill would be announced very soon.

UPDATE: The effective date of Finance Act, 2020 is on the 1st of February, 2020.

In addition to providing clarity to old and inexplicit policies, the newly signed bill has severe implications for businesses in Nigeria and the citizens at large. Some of these implications are as follows;

1. Company Income Tax (CIT) and the Finance Act, 2020

Commencement and cessation rules have been modified in such a way that overlaps and gaps have been discontinued. Therefore, CIT 29 (3) and (4) have been replaced. This was done to prevent double taxation on the same income due to overlapping periods, and avoid the complications that arise during commencement.

Additionally, a company that is yet to commence business no longer need to pay pre-operation levy while applying for Tax Clearance Certificate. The payment of CIT can now be made in one lump sum or in installments, on or before the due date of filing.

Benefit

This is advantageous to new businesses because they won’t be double taxed on the same income in the first and second year of starting a business. The preceding year is now used as the basis period. Hence, the first year of assessment is no longer deemed by the finance act as the year of commencement of business.

2. The Implications of Finance Act, 2020 on Businesses in Nigeria

Companies are now categorized into three financial segments;

A. Small and medium scale enterprises with less than N25 million revenue will be exempted from paying Company Income Tax (i.e., CIT is 0%);

B. Medium sized companies with a turnover between N25 million and N100 million will pay Company Income Tax at a lower rate of 20% (i.e., CIT is 20%); and

C. Big companies with a revenue above N100 million will continue to pay the 30% Company Income Tax (i.e., CIT is 30%).

Explanation

It is pertinent to note that the law only grants the incentives of 0% and 20% respective tax rates to SMEs and medium sized companies who disclose their returns. Nonetheless, the Act does not exempt their returns from Tax Audits and Desk Examinations. Any suppression of income will be addressed.

Benefit

Therefore, small and medium scale enterprises within the first category enjoy a tax relief provided by the Finance Act of 2020. This will encourage them to come forward and disclose their revenue to the appropriate tax bodies to enjoy the benefits of such disclosure.

3. Bonus on Early Payment of Company Income Tax

If the company income tax of a firm is paid 90 days before the due date for tax payment or 3 months after the end of the company’s accounting year, it is entitled to receive a bonus of:

A. 2% of the tax payable for a medium sized company. A medium sized company as stated earlier is a firm with an annual turnover between N25million and N100 million

B. 1% for any other company (big companies). Early payment for such companies will be 29% instead of 30%.

Since small companies have a 0% tax rate, no bonus is accruable to them. Even at that, late submission of their tax returns documents would attract a penalty. Therefore, in order to avoid facing legal sanctions all companies are advised to file before the due date.

4. Impact of the Finance Act, 2020 on Insurance Companies

Insurance companies, like other businesses, are now allowed to indefinitely carry forward their losses.

Explanation

Prior to the implementation of the 2019 finance bill insurance companies were allowed to carry forward their losses for a maximum of four years, after which any losses recouped are viewed to have lapsed.

Benefit

Operators in insurance sector will enjoy relief on their losses like companies in other sectors.

5. Dividend and the Newly Signed 2019 Finance Bill

While applying the excess dividends tax law under the provision of Section 19 of CITA, retained earnings already subjected to tax are to be exempted.

Explanation

Prior to the signing of the Finance Bill, 2019 into law, when the dividend distributed to shareholders are greater than the chargeable or total profits of the business, the dividend paid out was deemed to be the chargeable profit and tax at a rate of 30%.

Since the residual income (retained earnings) available to shareholders has been taxed, and dividend is paid out of the company’s residual income, charging tax on the dividend paid out means taxing an after-tax income, which leads to double taxation.

Benefit

This provision will favour shareholders because their incomes will no longer be taxed twice.

6. Non-Resident Companies and the Finance Act, 2020

Minimum tax computation has been amended to 0.5% of gross turnover. The minimum tax provision only affect companies with a turnover of N25 million and above, because companies with a turnover below N25 million are exempted from Company Income Tax. Hence, companies with imported share capital of 25% are no longer exempted from minimum tax.

Prior to the implementation of the Finance Act, 2020 the minimum tax computations were a higher of;

A. 0.5% of Gross Profit;

B. 0.5% of Net Assets;

C. 0.25% of paid up capital;

D. 0.25% of revenue (turnover).

In addition, for companies with turnover higher than N500,000;

E. 0.125% of revenue in excess of N500,000.

7. Valued Tax Added (VAT)

VAT rate has experienced a 50% increase from 5% to 7.5%. The items exempted from VAT include cooking oil, milk, nuts, flour and starch, fruits, live or raw meat and poultry, roots, salt, vegetables, culinary herbs, fish of all kinds, locally manufactured sanitary towels, tuition and services rendered by Microfinance Banks.

According to Act the threshold for taxable persons set at N25 million. This means that micro, small and medium scale enterprises (MSMEs) with a turnover below N25 million have been exempted from VAT registration. Hence, they do not have the duty to invoice and collect VAT.

In addition, VAT Returns are to be rendered on cash basis instead of accrual basis. The Finance Law has introduced a “Self Charge Provision” to ensure payment of VAT on all supplies even when invoiced.

8. Stamp Duties

Stamp Duty of N50 shall apply on bank transfers only on amount from N10, 000 and above.

Benefit

Bank transfers and other online transactions below N10, 000 are exempted from Stamp duties. Transfers between the same owner’s accounts in the same bank are also exempted irrespective of the amount.

9. Petroleum Profit Tax (PPT)

Section 60 of the Petroleum Profit Tax Act has been redacted. Therefore, the dividend paid out of PPT to individuals or corporate entities (under the Personal Income Tax regime) is now subject to 10% Withholding Tax.

Before now the PPT Act exempted such dividends from tax.

10. Communication With Tax Authorities

E-mail communications with the tax authority is now accepted as a valid means of communication.

Benefit

This provision makes communication with tax authorities easier than before.

11. Fees on Technical Services

Fees on technical services payable to a non- Nigerian company without a fixed base in Nigeria is now chargeable to a withholding tax rate of 10%.

12. Interest on Loan

Interest on loan from a connected or related party is allowable up to 30% of Earnings Before Interest (EBIT).

13. Redefinition of Goods and Services

The definition of goods and services has been expanded to cover all forms of supplies, tangible or intangible except money or securities.

14. Failure to Notify the Service of a Change of Business Address

Failure to notify the Service of a change of business address or permanent is liable to penalty of N50,000 in the first month and N25,000 each in the subsequent months.

15. Tax Identification Number

Individuals now need to have a Tax Identification Number (TIN) before they can open a business bank account. However, existing owners of business accounts must provide a TIN to continue bank operations.

Highlights of the Finance Act, 2020

- New businesses will no longer be double taxed on the same income on overlapping periods within the first and second year of starting a business.

- A company that is yet to commence business no longer need to pay pre-operation levy while applying for Tax Clearance Certificate.

- Small and medium scale enterprises with less than N25 million revenue will be exempted from paying Company Income Tax. While medium size companies with a turnover between N25 and N100 million have experienced a tax reduction from 30% to 20%.

- Operators in the insurance sector will enjoy relief on their losses like companies in other sectors.

- Bank transfers and other online transactions below N10, 000 are exempted from Stamp duties.

- Apart from corporate bodies, Nigerians who want to open or maintain bank accounts do not need to provide their Tax Identification Number (TIN).

- The acceptance of email as a means of communication makes communication with tax authorities easier than before.

- The increase of VAT from 5% to 7.5%.

Zerofy Editorial is a team of writers determined to provide evergreen content to millions of readers worldwide.